Helping You To Better, Brighter Future

Better Futures Club is committed to helping people and families take control of their finances.

Budgeting – especially on a low or variable income or while dealing with debts – is challenging, but it’s achievable with the right strategies.

We’ve gathered expert tips on budgeting and money management, with advice tailored for UK households.

You might be struggling to manage your money if…

Your income changes month to month

such as zero-hours work, self-employment, shift work, or fluctuating benefits, making it hard to plan ahead.

Rising bills and everyday costs

mean your money runs out before the end of the month, even though you’re careful with spending.

Debt repayments are piling up

and it feels like you’re juggling credit cards, overdrafts, or loans just to keep going.

Unexpected costs keep knocking you off track

like car repairs, school expenses, or replacing broken essentials, leaving you stressed and scrambling.

Managing your money better can help by…

Giving you clarity and control

so you know what money you have, what needs paying first, and what’s left — even when income isn’t steady.

Reducing stress and worry

by helping you stay on top of bills, avoid missed payments, and plan for the month ahead.

Breaking the cycle of debt

by prioritising essential costs, spotting ways to reduce spending, and finding safer, fairer finance options like credit unions.

Building a small safety cushion

so unexpected costs don’t turn into financial emergencies and you can feel more confident about the future.

Not Already A Member? Join Today

Services

Step-by-Step Into A Better, Brighter Future

How it works

Money Management In Detail

01

Calculate Your Income

Add up all the money you receive in a typical month. Include wages (after tax), benefits, pensions, maintenance payments – every source of income . If your income varies each month, it’s safest to budget based on your lowest monthly income so you’re not caught short in a bad month . Another approach is to calculate your average monthly income (sum up the last 12 months and divide by 12) . When you have a good month, don’t splurge the extra – consider saving it to cushion the lean months . • Visual tip: If your income fluctuates, you might include a small chart or graph showing a few months of high and low income, with a line for the “safe” budget level (the lower-income figure). This can illustrate why budgeting conservatively helps avoid shortfalls.

List All Your Expenses

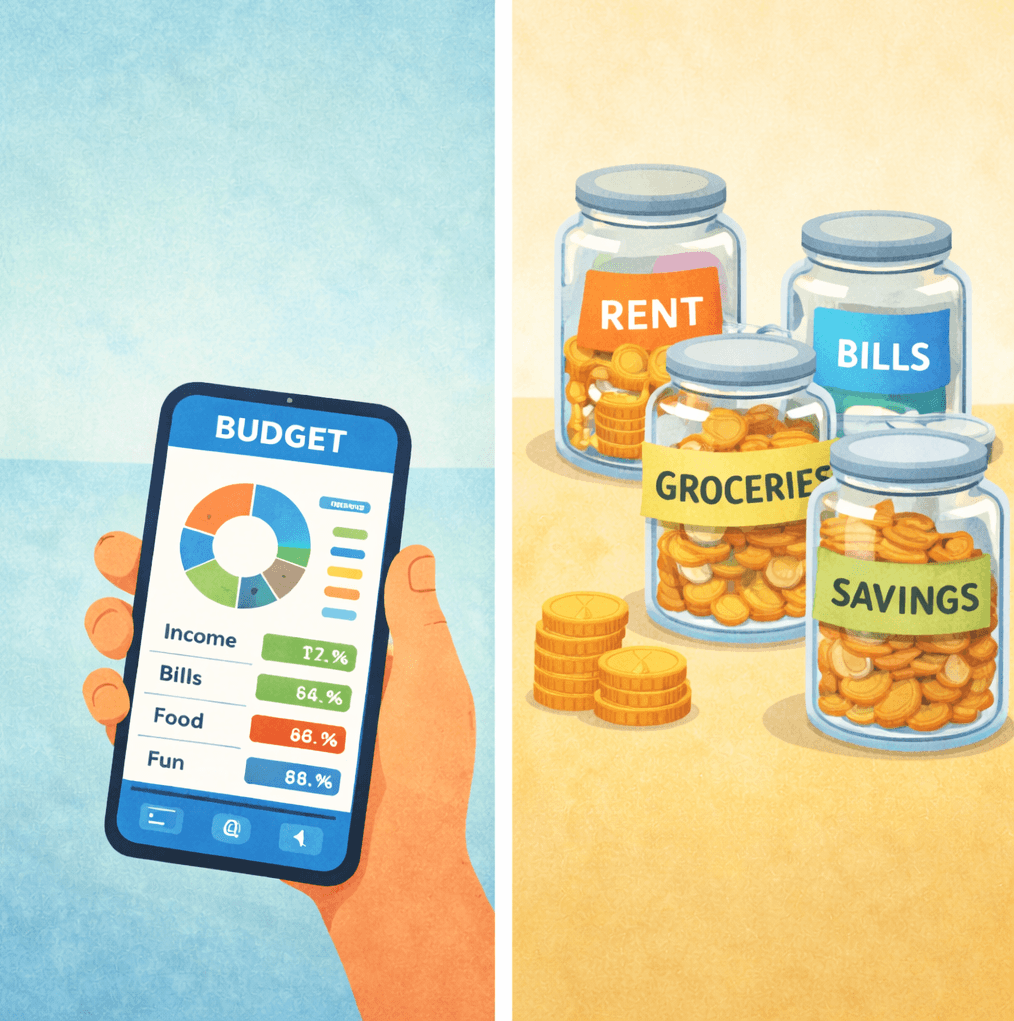

Write down everything you spend money on in a month . It helps to break expenses into categories: • Essential living costs (Needs): rent or mortgage, utility bills (gas, electricity, water), Council Tax, groceries, transport to work or school, insurance, child care costs . These are expenses you must pay to keep a roof over your head, stay safe and get to work. • Financial commitments: loan repayments, credit card minimum payments, phone bills, TV/internet subscriptions – any regular bills or debt payments . • Everyday living (Wants): discretionary spending like entertainment, dining out, gym memberships, hobbies, or takeaways. Also include occasional treats for yourself or the kids. These are optional expenses you can trim if needed . • Irregular and annual costs: those expenses that don’t occur every month. Think of birthdays, Christmas gifts, holidays, car maintenance or MOT, school uniforms, and other one-offs . Add up what you expect to spend in a year on these and divide by 12 to put a monthly amount in your budget . This way, you’ll set aside a bit each month toward those costs instead of scrambling when they arrive. Pro Tip: Prioritize “must-pay” expenses (priority bills) first. In the UK, certain bills have serious consequences if not paid. Priority debts include rent or mortgage, energy bills, Council Tax, and court fines – if these aren’t paid, you could lose your home, have your power cut off, or even face legal action . Make sure your budget covers these critical expenses before anything else. Less urgent bills (like credit cards or streaming services) should be dealt with after the essentials . A handy tool is MoneyHelper’s Bill Prioritiser, which can show you which payments to tackle first . • Visual idea: Consider a pie chart showing expenses by category (housing, bills, food, etc.). This can illustrate where most of the money is going. Another idea is an image of stacked jars or envelopes labeled for rent, bills, food, etc., highlighting the “jam jar” budgeting method (explained below).

02

03

Choose a Budgeting Method

It doesn’t matter whether you use a fancy app, a spreadsheet, or pen-and-paper – use whatever method you find easiest to track your budget . Many people start with simple tools and gradually refine them. Here are a few approaches: • Traditional Spreadsheet or Notebook: Write down your income and all expenses in a notebook or use a spreadsheet template. This low-tech method works well and can be easily updated. (You can embed a snapshot of a basic budget table or use an illustration of a notebook with budget items.) • Budget Planner Tools: Try free online tools like the MoneyHelper Budget Planner , which adds up your income and outgoings and shows you what’s left. These tools often give personalized tips on where to cut back once you input your details . There are also smartphone apps that sync with your bank to track spending automatically (just ensure any app you use is reputable and secure). • Envelope or “Jam Jar” Method: This is a visual way to manage money – perfect if you prefer something tangible. Divide your cash into separate pots or envelopes for each spending category . For example, you might have an envelope for groceries, one for travel, one for leisure. When each envelope (or jam jar) is empty, you’ve hit the limit for that category. Digital version: Some bank accounts let you create multiple sub-accounts or savings pots to partition your money for bills, savings, etc. . This method, often called piggybanking, helps prevent accidentally spending the rent money on nights out – you always know the essentials are covered .

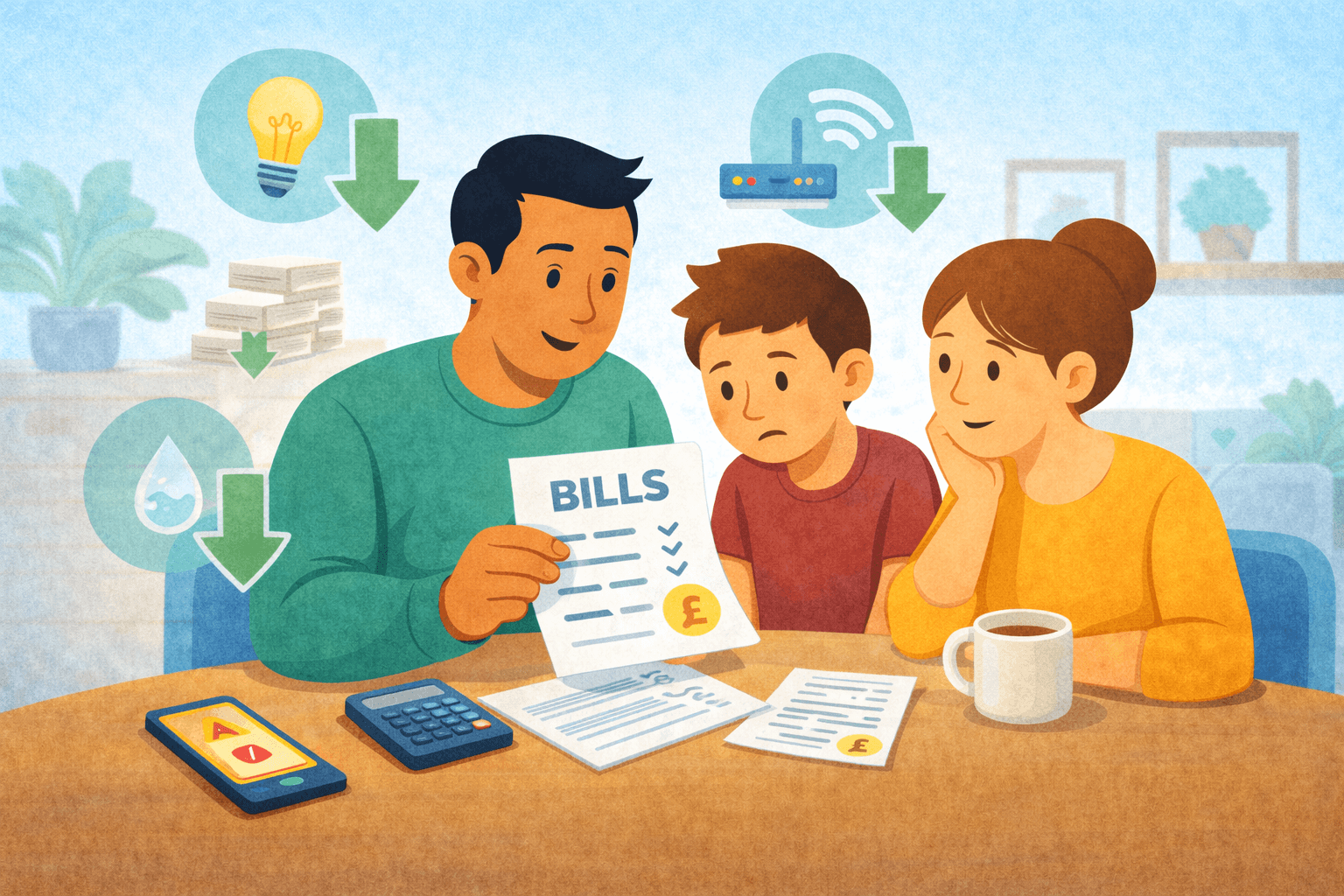

Lowering Your Everyday Bills and Essentials

Many of the biggest savings come from regular bills and everyday costs — things you pay month after month. Things to focus on: • Household bills: Check whether you’re on the best deal for energy, broadband, and mobile. If you’re out of contract, you may be able to switch or negotiate a better price. • Discounts and support schemes: If you’re on a low income or certain benefits, you may qualify for help like the Warm Home Discount or water bill support schemes. • Energy use at home: Simple actions like turning the thermostat down slightly, switching off appliances at the wall, and using less hot water can make a noticeable difference over time. • Ask for help early: If you’re struggling to pay a bill, contact the provider as soon as possible. Many companies can offer payment plans or point you towards support or hardship funds. Why this helps: Lowering essential bills frees up money for food, transport, savings, or paying down debt — without cutting back on things that really matter

04

05

Spending Smarter on Food, Transport, and Daily Life

Day-to-day spending is where lots of small savings can quietly add up. Things to focus on: • Food and groceries: Plan meals for the week, write a shopping list, and stick to it. Own-brand products and cheaper supermarkets often offer the same quality for less. • Avoid impulse spending: Shopping when hungry or tired can lead to overspending — planning ahead really helps. • Transport: Check if weekly or monthly public transport passes are cheaper. If you drive, simple maintenance can improve fuel efficiency. Walking, cycling, or car sharing can save money too. • Use free or low-cost options: Libraries, parks, community events, and free museums can replace more expensive outings — especially helpful for families. Why this helps: Smarter everyday choices can reduce pressure on your budget without feeling like you’re constantly missing out.

Cutting Back on Subscriptions and Extras

Subscriptions and small “extras” can quietly drain money without you noticing. Things to focus on: • Review subscriptions and direct debits: Cancel anything you don’t use or could pause for a while — streaming services, gym memberships, apps, or magazines. • Be flexible: You can often re-subscribe later when your finances feel more stable. • Think short-term for long-term gain: Even a temporary pause can free up cash for essentials, savings, or reducing debt. Why this helps: Cutting back on extras gives you breathing room and helps you focus on your bigger goals, like building savings or clearing debts.

06

07

Make Sure You’re Getting All the Support You’re Entitled To

Many people miss out on financial help simply because they don’t know it exists or assume they won’t qualify. Things to explore: • Check your benefit entitlements: A quick benefits check can show whether you’re entitled to support like Universal Credit, Child Benefit, council tax reductions, or disability benefits. • Look for grants and local support: If you’ve had an income shock (job loss, illness, reduced hours), there may be charitable grants or local council hardship funds that can help with specific costs. • Short-term help when things are tough: Food banks, school uniform support, and community support schemes exist to help people through difficult periods. Why this helps: Support and grants don’t need to be paid back and can ease pressure straight away, helping you stay on top of essentials.

Finding Ways to Bring in Extra Income

Even small amounts of extra income can make a big difference to your monthly budget. Things to explore: • Increase take-home pay: Check if overtime or extra shifts are available, or whether flexible or part-time work could fit around your life. • Sell what you no longer need: Decluttering your home and selling unused items online or at a car-boot sale can bring in quick cash. • Use your skills or hobbies: Things like tutoring, DIY help, baking, dog walking, or creative work can bring in extra money when done at your own pace. Why this helps: Extra income can help cover rising costs, reduce reliance on credit, and create space for saving or paying down debt.

08

09

Make Sure You’re Getting All the Support You’re Entitled To

Many people miss out on financial help simply because they don’t know it exists or assume they won’t qualify. Things to explore: • Check your benefit entitlements: A quick benefits check can show whether you’re entitled to support like Universal Credit, Child Benefit, council tax reductions, or disability benefits. • Look for grants and local support: If you’ve had an income shock (job loss, illness, reduced hours), there may be charitable grants or local council hardship funds that can help with specific costs. • Short-term help when things are tough: Food banks, school uniform support, and community support schemes exist to help people through difficult periods. Why this helps: Support and grants don’t need to be paid back and can ease pressure straight away, helping you stay on top of essentials.

Building an Emergency Fund (Even a Small One)

When money is extremely tight, saving might seem impossible. But even a small emergency fund can be a lifesaver when unexpected costs hit. Start with very modest goals: try to save £5 or £10 a week if you can, or put aside any little windfalls (like a birthday gift, a tax rebate, or spare change in a jar). Over time, these bits of money grow into a buffer. Why is an emergency fund important? Because it prevents one emergency from turning into debt. If the cooker breaks or you need an urgent car repair, having some savings means you don’t have to resort to high-interest credit or go into arrears on other bills. Ideally, aim for 3 months’ worth of essential expenses saved up eventually , but if that sounds huge, start with a goal of £500, then £1,000. Even one month’s rent or one month’s income in the bank is a big safety net . Treat saving like a bill to pay to yourself. When budgeting, include a line for “Savings” – even if it’s small. Set up a standing order on payday to transfer £X into a savings account (this works well because you don’t “miss” money you never see in your spending account). Some banks offer “round-up” features (they round your debit card purchases to the nearest pound and move the spare pence into savings) – it’s an effortless way to save small amounts. Remember, emergency savings are for true emergencies – not for planned annual costs (those should be in your budget as discussed) and not for splurges. Keep this fund in an easy-access savings account so you can withdraw it quickly if needed, but try to leave it untouched except for real emergencies. If you do need to dip into it, prioritize rebuilding it afterward.

10

Contact us

Want to reach out to us?